In our Q2 Market Note, we examine a market environment defined by disruption, from shifting Federal Reserve policy and persistent inflation to AI-driven productivity, energy volatility, and resilient global equity markets. While uncertainty remains elevated, the note emphasizes the importance of staying invested near long-term targets while maintaining added liquidity and caution.

Please read the full text below or download the PDF version.

Executive Summary

- President Trump’s Federal Reserve Chair nominee, Kevin Warsh, noted in his Senate confirmation hearings that “(t)his is the most disruptive moment in modern economic history in the US and the world.”[i]

- Although he was referring specifically to artificial intelligence (AI), in 2026, one can argue that it applies more broadly to the world and markets. Despite “SaaSpocalpyse” and the “largest energy supply shock in history”, markets have surprisingly jumped higher.

- Disruptive forces are working in many directions. Some are creating worry and volatility; others are creating remarkable new technologies and opportunities. We continue to advise clients to stay invested near targets with some added liquidity and caution.

Cash and Bonds

Starting with cash in US dollars, the forces controlling the all-important cost of money are undergoing dramatic disruption. First, we have the unprecedented and politicized drama surrounding Warsh’s confirmation itself. Democratic Senator Elizabeth Warren’s barbed questions to Warsh were expected[ii]. Republican Senator Thom Tillis’ threat to block Warsh’s nomination until Trump’s Department of Justice (DoJ) dropped its investigation into Jerome Powell, Trump’s former nominee and current chair, was unprecedented.

While Trump and the DoJ have backed down for now[iii], clearing the path for Warsh’s nomination, the Fed still faces disruptive forces. For one, Chair Powell is bucking tradition and plans to stay on the board citing the “unprecedented legal attacks”[iv] on the central bank’s independence. He and many others rightly see the Fed’s independence from politics as one of the crown jewels that has made America special.

Next, inflation has run above the Fed’s 2% target for five years now and recently accelerated to its fastest pace in three years. While the market has moved from pricing in two Fed rate cuts to potentially one rate hike in 2026, Warsh thinks the Fed can still cut rates. He thinks that trimmed inflation excluding major outliers is more appropriate[v] and that AI will unleash a wave of disinflationary productivity. While he sees himself as a young Alan Greenspan[vi] who saw the same disinflationary forces in the internet, he must contend with a Fed experiencing its highest level of dissent in over three decades[vii]. He must convince this board, including Powell, to abandon Powell’s cautious data-driven “navigating by the stars under cloudy skies”[viii] and rough seas approach for his “guess” that AI “is the most productivity-enhancing wave of our lifetimes.”[ix]

Warsh shortly will arguably become one of the most followed people on earth and the world will be watching him closely. Whether he goes down like the Maestro, Alan Greenspan, orchestrating the global economy smoothly through these disruptive forces or like Nixon’s sock puppet, Arthur Burns, who nearly ruined the US dollar and the Federal Reserve is an open page before us. For now, we think neither extreme is likely and turn to bonds to explain why.

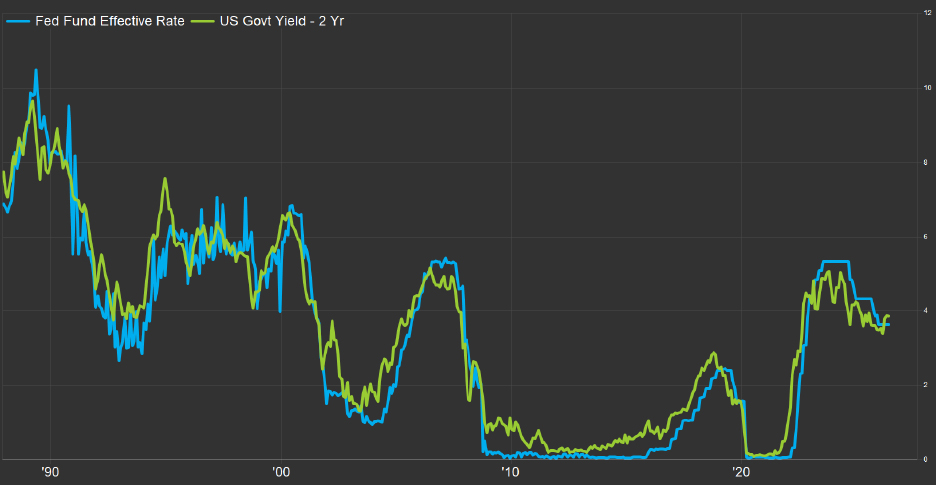

While Warsh may become one of the most listened to voices on earth, we are reminded of a quote from President Clinton’s political adviser James Carville. Following the “Great Bond Massacre” of 1993-1994 where the 10-year US Treasury yield jumped from 5% to 8% on deficit concerns, Carville noted “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”[x]

Alan Greenspan, who led the Fed at the time, hiked the Fed Funds rate from 3% to 6% and Clinton and Congress steadily shrank the deficit from ~4% of GDP to a fiscal surplus by 1998. At the end of this note, we’ve included a chart of the 2-year US Treasury yield, Carville’s bond market, and the Federal Funds Rate. If you look closely, you will note that historically the bond market was ahead of the Fed and the Fed, even the Maestro, eventually followed the intimidating market. Today the market is saying the Fed should be closer to 4%, that one 2026 rate hike we noted earlier. We think these forces will guide the Fed for now.

On the fiscal side, rising bond yields and warnings from respected investors have yet to intimidate our profligate government into reducing the deficit. While no one is calling it a bond massacre yet, the 10-year US Treasury yield has jumped in five years from 1.6% to 4.4% today with inflation consistently above the Fed’s targets. In terms of disruptive forces, US bonds are no longer behaving as a safe asset and fell again amidst the market turmoil in March. Despite these ructions, US fiscal deficits continue to run at unprecedented levels outside of wars and recessions. The current ~6% deficit to GDP is expected to worsen given tax cuts from the One Beautiful Bill (OBB), rebates from voided tariffs, and a record setting $1.5 trillion proposed military budget.

Numerous respected investors have warned about these deficits as far as the eye can see. Former Treasury Secretary and investor Hank Paulson recently warned that the US needs “an emergency break-the-glass plan”[xi] should another bond massacre occur. At Berkshire Hathaway’s recent annual meeting, Warren Buffett expressed serious concerns around US debts and deficits, highlighted that runaway inflation is a common phenomenon and that we are “not immune from it happening.”[xii] Buffett noted that we came close to losing control under Arthur Burns, but credited Paul Volker (and we’d add the personal computer and baby boomer savings) with bringing us bank from the brink.

We tend to agree with Churchill’s quote here that “(y)ou can always count on Americans to do the right thing, after they have exhausted all other possibilities.” The US seems to be in the exhausting possibilities phase now. We don’t mind tilting more toward ~4% cash and away from 4.5% longer-term bonds for now with 3+% inflation. Interestingly, the Fed has quietly been growing its balance sheet by buying US Treasuries since the end of last year. While Warsh has spoken against balance sheet expansion recently, this may in fact be part of the “break-the-glass plan” required should bond yields shoot higher.

Global Stocks

On the bright side, relatively cheap and abundant liquidity, fiscal deficits and other disruptive forces have largely benefited the stock market for now. Despite the war in Iran and the resulting 67% year-to-date jump in oil prices which typically have hurt the economy and equities, US GDP grew at 2% in Q1. US stocks finished the quarter down just 5%. In April, US stocks jumped over 10% staging their fastest recovery ever from a 10% loss or greater and now stand back at record highs.

Propelling this rebound were earnings which to date have grown at a remarkable 27% year-over-year to date[xiii] for the S&P 500. Earnings have certainly been supported by lower taxes from the OBB but are also coming from AI with the “Magnificent 7” companies reporting 61% year-over-year growth. Weekly AI token consumption quadrupled between January and March.[xiv] Much of this was driven by Anthropic’s Claude coding capabilities and CEO, Dario Amodei, just noted that his company may grow 80X year-over-year.[xv] He noted that such growth was difficult to manage and this may be another reason besides being “too dangerous” why its highly advanced Mythos model was released on a limited basis.

While valuations remain historically rich at 21X forward earnings, this type of earnings growth is unprecedented outside of recession recoveries. While we remain slightly underweight US equities due to these heightened valuations, we remain close to target. We also continue to like small and mid-cap stocks given their fairer valuations. Small and mid-cap earnings growth has also been strong, and year-to-date returns have strongly outpaced large caps. Both Paulson and Buffett also highlighted American exceptionalism. Should Warsh’s best guess as to what AI will usher in prove prescient, investors will need to own AI stocks as BlackRock’s Larry Fink noted.[xvi]

While most of the international markets in Europe and China are composed of energy importers which also typically struggle with surging energy prices, international markets were also resilient to 2026 disruptions to date. While international stocks fell 10% in March, they finished the quarter flat after their hot start. They also experienced a rapid recovery with a 10% jump in April and have outpaced US stocks year-to-date. While international earnings growth has been less exceptional, international stocks trade closer to their long-term average of 15X earnings.

The AI theme has also kicked in internationally with South Korea’s semiconductor-heavy index up over 70% year-to-date. In robotics and automation, Japan Airlines plans to use baggage-handling robots, while Gatwick airport is testing autonomous wheelchairs.[xvii] A Chinese-made robot beat the human half-marathon record[xviii] while Chinese EV exports in March jumped 140% year-over-year. While we worry that Europe is falling behind with these high-tech adoptions given their fractured and regulatory environments and have similar concerns around the debt and deficits of many international countries, we continue to advocate for a near-neutral stance on international stocks.

Alternative Assets

With global markets up ~10% as of this writing, most directional hedge fund indexes, that move with the market, are up just mid-single digits, which just is not enough. In our opinion, too many hedge funds rely on “risk” models that cut risk during a drawdown and then fail to recoup commensurate gains in the ensuing rebound. When we add fees, illiquidity, and legal agreements that essentially allow these managers to do as they please, the juice is usually just not worth the squeeze. While we are pleased with most of the funds we own and our directional fund’s performance over the past several years, we continue to set a very high bar for new hedge fund investments.

We do however maintain conviction in truly uncorrelated strategies and were very pleased that our uncorrelated investments delivered a small, but positive return in March when nearly every asset class save for energy declined. We continue to think this is an important asset to hold in a world filled with disruption. Many investors saw private credit as an uncorrelated return stream. This thesis was challenged in Q1 as investors asked for nearly $20B in redemptions but only received ~50% of this.[xix] The thesis behind private credit was further stressed as many software firms entered a deep bear market in Q1’s “SaaSpocalypse”. Many private credit firms saw software cash flows as long-term and durable, but this thesis may be disrupted with AI. We have seen this asset-liability mismatch movie many times before, most recently when illiquid real estate was bundled into “semi-liquid” funds. We think many software firms with AI capabilities, lightly leveraged balance sheets and forward-looking CEOs will thrive in this environment. We may wade into software-heavy private credit if yields approach the mid-teens we saw recently in real estate debt. For now, we value our liquidity in uncorrelated assets so that we can draw down on them in the event of a deeper drawdown amidst this disruption.

Finishing on the theme of disruption, we would be remiss not to touch on the elephant in the room with the International Energy Agency calling the 2026 energy crisis “the largest energy supply shock in history.”[xx] While we have extolled the value of owning energy assets in secure countries for some time, we think now may be one of the most precarious times to invest in energy. The daily standard deviation of West Texas Intermediate (WTI) front-month oil has jumped six-fold to $7.55 per barrel from a long-term historical average of $1.25 as we wake up each morning to headlines that vacillate between peace and war.

New energy investments that are critical to AI adoption must be made considering the widest range of potential outcomes in history. While energy firms are reporting record profits today, many are concerned and upset with the volatility introduced into the market. While roughly 13 million barrels of oil supply per day has been lost from the war, analysts expect roughly 5 million barrels of oil demand to disappear as consumers buy EVs and airlines cancel flights. Adding to volatility and as we’ve noted in the past, the old world order in many ways is fading. To wit, the United Arab Emirates just surrendered its 59-year membership to OPEC. Given all this uncertainty, we think a high degree of caution is warranted with new energy investments.

Conclusion

In summary, we agree with Kevin Warsh that the world is undergoing dramatic disruption. While some of these disruptions are worrisome and create substantial volatility, others are creating remarkable progress and opportunities. Amid this disruption, we continue to advise clients to have some added liquidity and caution while still sticking close to their long-term targets.

We had the pleasure of attending Berkshire Hathaway’s annual meeting again this year. Despite the worries Buffett noted above, he has consistently criticized “chrono-centrism” where investors believe they are living through one of the most chaotic times in history. At 95 years old, he has remarkably lived through nearly 40% of our country’s 250 years on earth. He constantly reminds investors of all the terrible, chaotic events that have occurred in that time and notes that living today in America is like winning the ovarian lottery. Despite current disruptions, the future generally has improved for America, the world and humanity, at large and it pays to stay invested.

Source: FactSet, Sentinel Trust

This material is published solely for the interests of clients and friends of Sentinel Trust Company, L.B.A. and is for discussion purposes only. The opinions expressed are those of Sentinel Trust Company management and are current as of the date appearing in this material and subject to change, without notice. Any opinions or solutions described may not be suitable for investments nor applicable to all scenarios. The information does not constitute legal or tax advice and should not be substituted for a formal opinion. Individuals are encouraged to consult with their professional advisors.

The material is not intended to be used as investment advice, nor should it be construed or relied upon, as a solicitation, recommendation, or any offer to buy or sell securities or products. Any offer may only be made in the current offering memorandum of a fund, provided only to qualified offerees and in accordance with applicable laws. Each type of investment is unique. This material does not list, and does not purport to list, the risk factors associated with investment decisions. There can be no assurance that any specific investment or investment strategy will be profitable and past performance is not a guarantee of future investment results. Before making any investment decisions, you should carefully review offering materials and related information for specific risk and other important information regarding an investment in that type of fund.

Information derived from independent third-party sources is deemed to be reliable, but Sentinel Trust cannot guarantee its accuracy of the assumptions on which such information is based.

[i] https://www.nytimes.com/live/2026/04/21/business/kevin-warsh-fed-chair-hearing#:~:text=Live%20Updates:%20Trump’s%20Pick%20to,lives%20of%20the%20American%20people

[ii] https://www.youtube.com/watch?v=-GV8uCmA1ZE

[iii] https://www.wsj.com/economy/central-banking/justice-department-will-end-probe-of-powell-clearing-path-for-kevin-warsh-e6774dfa?mod=Searchresults&pos=10&page=1

[iv] https://www.youtube.com/watch?v=8os0vhVTiSQ

[v] https://www.cnbc.com/2026/04/22/kevin-warsh-inflation-trend-pce-trump.html

[vi] https://www.washingtonpost.com/opinions/2026/04/13/fed-chair-nominee-kevin-warsh-alan-greenspan-rates/

[vii] https://www.cnbc.com/2026/04/29/fed-interest-rate-decision-april-2026.html

[viii] https://www.federalreserve.gov/newsevents/speech/powell20230825a.htm

[ix] https://www.youtube.com/watch?v=6LtRcC-JgBI&t=60s

[x] https://en.wikipedia.org/wiki/Bond_vigilante#cite_note-bloomberg-1

[xi] https://www.bloomberg.com/news/articles/2026-04-16/henry-paulson-suggests-us-make-a-break-glass-treasuries-plan

[xii] https://www.cnbc.com/2026/05/02/cnbc-transcript-berkshire-hathaway-chairman-warren-buffett-sits-down-with-cnbcs-becky-quick-during-the-2026-berkshire-hathaway-annual-meeting-today-.html

[xiii] https://insight.factset.com/three-magnificent-7-companies-push-sp-500-earnings-growth-to-highest-level-since-2021

[xiv] https://www.economist.com/leaders/2026/04/30/the-ai-supply-crunch-is-here

[xv] https://www.nytimes.com/2026/05/06/technology/anthropic-ceo-ai-growth.html

[xvi] https://www.wsj.com/finance/investing/larry-finks-warning-invest-or-risk-getting-left-behind-by-ai-d2f1d09d

[xvii] https://www.economist.com/the-world-this-week/2026/04/30/business

[xviii] https://www.reuters.com/sports/humanoid-robots-race-past-humans-beijing-half-marathon-showing-rapid-advances-2026-04-19/

[xix] https://www.businessinsider.com/private-credit-20-billion-redemption-data-blue-owl-blackstone-apollo-2026-4#:~:text=Investors%20asked%20to%20take%20out,either%205%25%20or%207%25).

[xx] https://www.iea.org/data-and-statistics/data-tools/2026-energy-crisis-policy-response-tracker